A 15-page Morgan Stanley note has drawn a direct line between humanoid robots and the early days of electric vehicles. Its headline take: humanoid robots may well be the next industry catapulted forward by China, even capable of lifting the country’s global export share from 15% to 16.5%.

That’s not a wild guess. The report lines up a striking comparison — the current export scale of China’s humanoid robotics sector, it says, is roughly where Chinese EV exports were in 2019. What happened next is well known: EV exports went on a tear, eventually reaching an annualized $86 billion.

In other words, the clumsy machine you see hauling boxes in a warehouse, inspecting power plants or carrying trays in a fast-food joint could well be the BYD of five years ago. The story sounds fanciful, except it’s already playing out on factory floors in Shenzhen. It also suggests the humanoid robot industry is beginning to morph from an “AI play” into “advanced manufacturing.”

A lap ahead before the starting gun

How strong is this sense of a future already arriving? Morgan Stanley offers a number: roughly 90% of humanoid robots shipped globally in 2025 carried a Made-in-China label. While other countries are still wrestling with prototypes in the lab, Chinese robots are clocking in for work.

That’s only the part of the iceberg above the water. A separate McKinsey report turns over the much larger piece beneath the surface — the supply chain. It describes the humanoid robot supply chain as “the most underestimated bottleneck” and, at the same time, the most significant opportunity in decades.

For two decades the world has chronically underestimated Chinese manufacturing, often reducing it to “cheap.” What the robotics sector is now proving is that China’s real advantage was never low prices — it is industrial ecosystems and the supply chain spillover they create. That means at the very moment the global robotics industry is getting off the ground, China already sits on a ready-made industrial base. This is the central logic for understanding China’s robotics ascent.

Put simply, building a machine that can walk and jump is one thing. Building a hundred thousand or a million of them a year, reliably, affordably and at quality, is an entirely different challenge that depends on a mature supply chain. Today the bill-of-materials (BOM) cost for a humanoid robot runs anywhere from $30,000 to $150,000. Everybody knows the number has to drop below $20,000 for mass adoption to become real. Companies like Unitree and Zhiyuan in China are already there.

China’s “asymmetric advantage”

Lay the two reports side by side and the logic snaps into focus.

Morgan Stanley sees five pillars behind China’s momentum: a national strategy mapped out years ago, heavy R&D spending (2.8% of GDP), the world’s largest pool of STEM graduates (3.57 million a year, more than four times the U.S. figure), and the willingness of local governments to deploy industrial guidance funds essentially willing to “burn money for the future.”

McKinsey keeps circling back to one additional factor: the closed supply chain loop.

It’s easy to forget that China just fought and won a global-scale industrial war over electric vehicles. The legacy is enormous. Batteries, motors, motor controllers, rare-earth permanent magnets — these core components and capabilities transplant directly into robots with what can fairly be described as asymmetric force. China controls about 90% of global rare-earth magnet processing capacity, and those magnets are the heart of high-performance motors.

Morgan Stanley’s numbers are blunt: a Chinese-made robot costs at least 20% less than an overseas competitor on average. That kind of cost advantage is something neither Europe, the U.S., Japan nor South Korea can replicate quickly.

The U.S. remains strong in the “AI brain” department — Boston Dynamics and Tesla retain deep technical reserves — but hardware manufacturing ecosystems are a weak spot. Tesla has been pushing suppliers to move operations out of China. Japan has deep industrial-robot roots but its humanoid robots rarely leave the lab; South Korea boasts the world’s highest robot density but a commercialization timetable that lags well behind China’s. Both countries can build samples; they can’t build scale. Once the race moves into the physical world, industrial capability tends to overtake algorithmic prowess. And the player with the most real-world deployment scenarios has the fastest learning curve — a frighteningly powerful flywheel now getting underway.

The supply chain’s Achilles’ heel

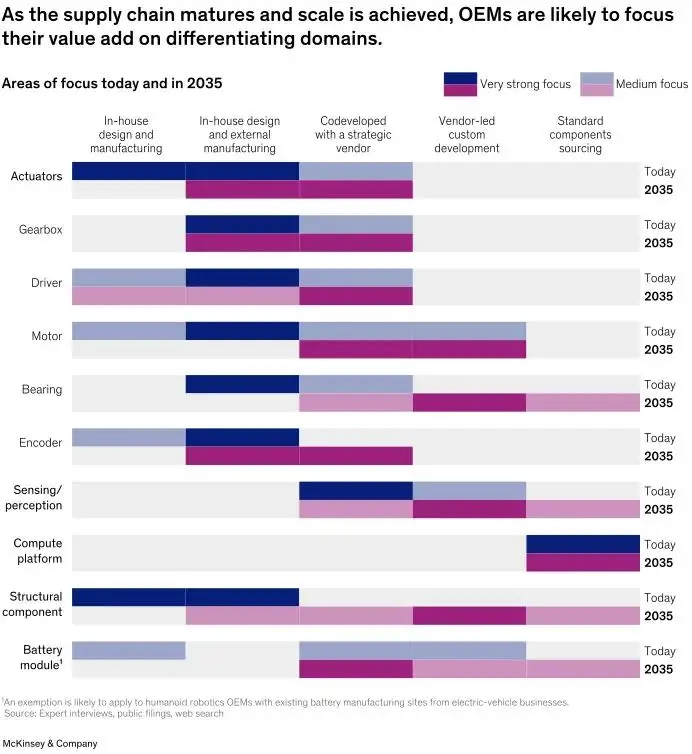

Here, though, lies what McKinsey calls a peculiar “mismatch”: actuators — which include motors, reducers and lead screws — determine the lion’s share of a robot’s performance and account for more than 50% of cost, yet they represent the least mature part of the supply chain.

McKinsey classifies risk into three buckets.

Low risk: components like batteries and brushless motors. These have already been churned out at massive scale by the EV and consumer electronics industries, and can be adapted with relative ease.

Medium risk: components where supply can be scaled but requires significant reengineering. This middle layer covers items already produced in volume in adjacent industries, but needing wider-reaching modification for humanoid robots. Encoders, certain real-time control electronics and IMUs (inertial measurement units) fall into this category — not all models deliver the latency, drift stability and fault tolerance required by dynamic bipedal balance. Vision hardware from autonomous-driving programs is often overspecified, too bulky or power-hungry for humanoid constraints, demanding substantial repackaging.

High risk: the real choke points. These are components that demand extremely high precision but lack any established high-volume supply base. They include six-axis force-torque sensors that give robot fingers a sense of touch, harmonic reducers and planetary roller screws for the joints. One requires exceptionally tight calibration processes; the other is capital-intensive and dependent on a small number of specialist manufacturers — such as Japan’s Harmonic Drive Systems — whose output can be constrained without warning.

This is why Tesla’s Optimus was designed with all 28 joint actuators built from scratch. It wasn’t a preference for vertical integration; Tesla simply couldn’t buy actuators off the shelf that met the performance requirements at the right price.

McKinsey calls this the “pre-modular phase,” where every robotics company is forced into vertical integration because the alternative is not surviving.

Who will become the “Bosch” of humanoid robots?

China, for its part, cannot afford to be complacent. Morgan Stanley flags the early signs of cutthroat competition. More than 150 companies are crowding the track, and China’s National Development and Reform Commission has already started warning about “homogeneous overcapacity.” McKinsey, however, sees a solution hidden in the supply chain’s next evolutionary step.

They predict that as volumes stabilise, vertical integration will give way to “platformization.” The analogy is the automotive industry: everyone builds their own engines only until a “Bosch of humanoid robots” emerges. Right now, every supplier with vision is trying to grab that spot.

Bosch itself has already moved, signing three humanoid robot drive-unit partnerships in half a year with the goal of generating 10% of group sales from this new field. Qualcomm has rolled out processors purpose-built for humanoid robots and is working with Figure AI and others to define the next-generation computing architecture. Even contract manufacturer Jabil is positioning itself as a scalable robot production platform.

The entry of these players is what will signal the real maturation of the global humanoid robotics supply chain.

The next decade’s globalization narrative

McKinsey’s report is sober; it makes clear nobody should be reaching for champagne just yet. Can humanoid robots work safely alongside humans without cages? How does the force-sensing and tactile supply chain scale? These questions demand joint action across the entire ecosystem — no single company can solve them alone.

Yet what Morgan Stanley sees from across the Pacific is a much grander storyline. Their assessment: humanoid robots are likely to face far milder trade barriers than electric vehicles. The logic is straightforward. EVs pose a direct threat to the century-old auto industries that are political sacred cows in Europe, the U.S., Japan and South Korea.

Robots? Many of those same countries are staring at labor shortages and aging populations. A capable, affordable robot starts to look less like a threat and more like a saviour. The report mentions that Audi has already begun working with China’s UBTECH in Europe — a German company becoming a customer. That sort of story would be almost unthinkable in telecoms or automotive equipment.

For that reason, the total addressable market (TAM) carries deep macroeconomic weight. Morgan Stanley projects: by 2036, global humanoid robot adoption will reach 24.4 million units. By 2040, it explodes to 137.9 million units. By 2050, the global installed base sits at 1 billion units; assuming a six-year replacement cycle, annual market revenue would reach an eye-watering $7.5 trillion.

That likely explains the conviction behind the report. This isn’t a simple story of industrial substitution. It’s about China systematically projecting the supply chain momentum, talent depth and market scale built over the past two decades onto a brand-new track, with the potential to redraw the rules of global manufacturing.

The risks are plain to see: reckless over-competition, stubborn technical bottlenecks, fragmented deployment scenarios. But in a race where the starting pistol hasn’t yet fired, the Chinese team has already completed its first lap. What matters now is whether the contestants can turn that head start from “can we build it” into “can we build it well — and profitably.”