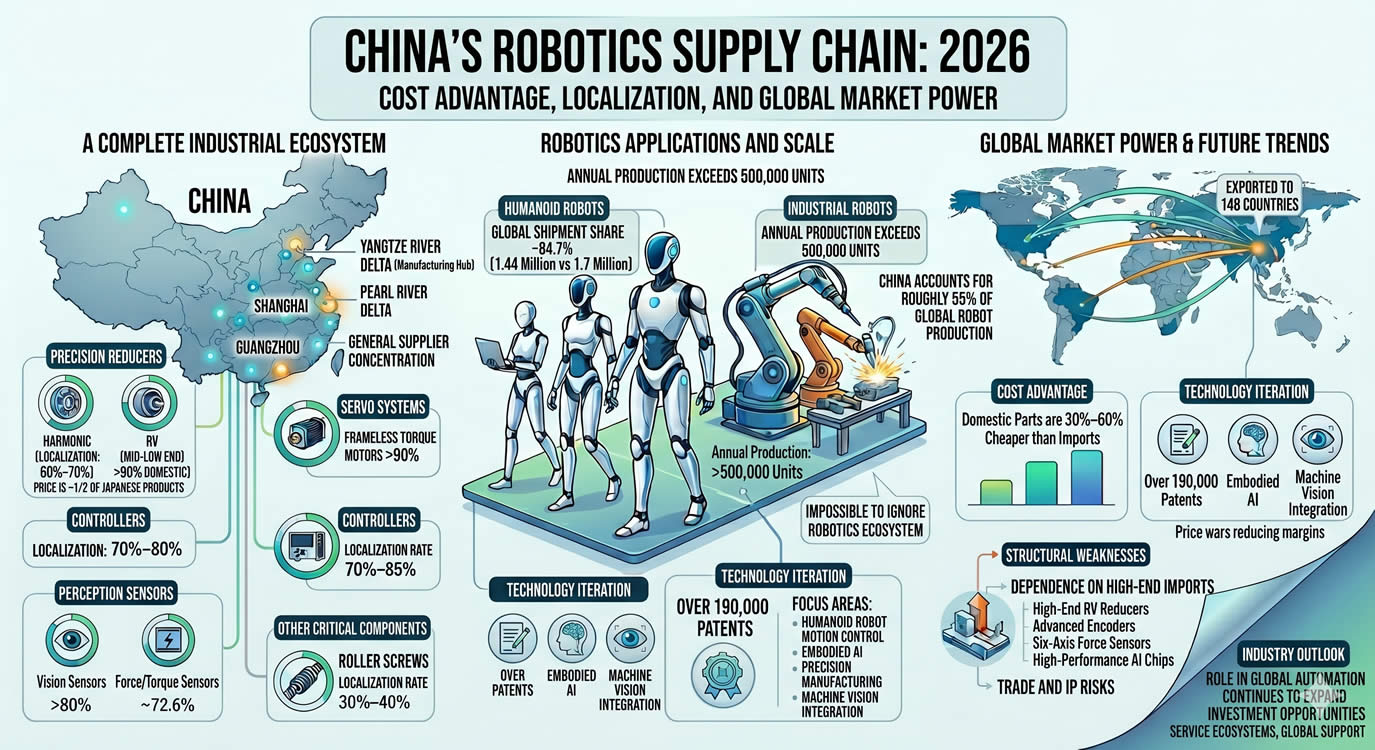

China’s robotics industry is no longer just a manufacturing base for overseas brands. In 2026, the country has built one of the world’s most complete robotics supply chains, covering everything from core components and motion systems to humanoid robots and industrial automation platforms.

Localization rates for key robotics components now range between 70% and 85%, while Chinese companies account for more than 84% of global humanoid robot shipments. In industrial robotics, domestic brands have captured 58.5% of China’s home market, marking a major shift from the import-dependent landscape of a decade ago.

For global investors and manufacturers, China’s robotics ecosystem has become impossible to ignore.

1. Why China’s Robotics Supply Chain Has Become Globally Competitive

1.1 A Complete Industrial Ecosystem

China now operates a full closed-loop robotics supply chain covering:

- Precision reducers

- Servo systems

- Controllers

- Sensors

- Actuators

- Robot assembly

- System integration

The concentration of suppliers in manufacturing hubs such as the Yangtze River Delta and Pearl River Delta has created a highly efficient industrial network.

Compared with overseas competitors:

- Local supply response times are typically 30%–50% faster

- Delivery cycles have shortened from three to six months down to one or two months

- Many component suppliers can support 24-hour rapid production coordination

This level of manufacturing integration has become one of China’s biggest structural advantages in robotics.

1.2 Cost Advantages Are Reshaping Global Pricing

Chinese robotics components are significantly cheaper than imported alternatives across multiple categories.

In many cases:

- Domestic components cost 30%–60% less than foreign equivalents

- Harmonic reducers are priced at roughly half the cost of Japanese products

- High-end force sensors have fallen sharply in price due to domestic competition

Scale is also playing a major role. China now produces more than 500,000 industrial robots annually and more than 50,000 humanoid robots per year. Together, Chinese manufacturers account for roughly 55% of global robot production volume.

For overseas buyers, China’s pricing advantage is increasingly difficult to match.

1.3 Faster Technology Iteration Through Large-Scale Deployment

China has become the world’s largest robotics application market, accounting for more than 45% of global industrial robot installations.

That scale gives Chinese companies access to massive amounts of real-world operational data and deployment scenarios, allowing products to improve faster through continuous iteration.

China also leads globally in robotics intellectual property filings, with more than 190,000 robotics-related patents — roughly two-thirds of the world total.

Key areas of progress include:

- Humanoid robot motion control

- Embodied AI

- Precision manufacturing

- Machine vision integration

The combination of manufacturing scale and live industrial deployment is accelerating product maturity across the sector.

1.4 Expanding Global Market Share

Humanoid Robots

Global humanoid robot shipments reached around 17,000 units in 2025. Chinese companies supplied approximately 14,400 units, representing an estimated 84.7% global market share.

Leading manufacturers include UBTECH Robotics, AgiBot, and Unitree Robotics. Chinese humanoid robots are typically priced 40%–60% below comparable Western systems.

Industrial Robots

Chinese domestic brands now hold 58.5% of China’s industrial robot market. Robot exports increased 42% year over year in the first quarter of 2026, with Chinese robotics products shipped to 148 countries.

However, international leaders including FANUC, Yaskawa, ABB and KUKA still maintain an advantage in some high-end industrial applications.

Consumer and Service Robots

Chinese brands dominate several consumer robotics categories:

- Cleaning robots: more than 70% global market share

- AGV and logistics robots: over 80% domestic share and more than 40% global share

China’s strength in consumer electronics manufacturing has helped accelerate growth in these segments.

2. China’s Robotics Core Components: Localization vs Imports

Core components account for more than 80% of a robot’s total manufacturing cost. Approximate cost breakdown:

- Reducers: 30%–35%

- Servo systems: around 25%

- Controllers: 10%–15%

- Sensors: 10%–15%

2.1 Precision Reducers

Harmonic Reducers

Used primarily in humanoid and collaborative robots. Localization rate: 60%–70%. Chinese global market share: around 26%. Japanese suppliers still control more than 60% of the global market.

Major Chinese suppliers include Leader Harmonious Drive Systems, Han’s Motion Technology, and Zhongda Leader. China still depends heavily on Japanese suppliers for ultra-high-end long-life harmonic reducers.

RV Reducers

Primarily used in heavy industrial robots. Mid- and low-end localization exceeds 90%, but high-end localization remains between 15% and 35%. Japanese company Nabtesco still controls more than 70% of the global RV reducer market. Chinese manufacturers currently hold roughly 10%–15%.

Key domestic players include Shuanghuan Transmission and Zhongda Leader.

Roller Screws

A critical component for humanoid robot linear actuators. Localization rate: 30%–40%. European suppliers still dominate more than 80% of the market. Chinese products currently account for roughly 10%–15% global share but are significantly cheaper — often around one-quarter the price of European alternatives.

2.2 Servo Systems and Motors

Overall localization rates remain between 25% and 50%. In frameless torque motors, localization has already exceeded 90%. Chinese brands currently hold approximately 20%–25% of the global servo market, while Japanese companies such as Yaskawa and Panasonic still dominate high-end applications.

One major weakness remains high-precision encoders, which continue to rely heavily on imports from Japan and Germany.

2.3 Robot Controllers

Localization rates for robot controllers have reached 70%–80%. Chinese companies now hold roughly 30%–35% of the global controller market. Major domestic suppliers include Estun Automation, Inovance Technology, and Siasun Robot.

Chinese controllers are increasingly competitive due to lower cost, faster local customization, better adaptation to domestic industrial scenarios, and stronger AI integration capability.

2.4 Perception Sensors

Vision Sensors

Including 2D cameras, 3D cameras and LiDAR systems. Localization rate: above 80%. Chinese suppliers hold more than 40% global market share. Leading companies include Hikvision and Orbbec.

Force and Torque Sensors

Localization has reached approximately 72.6%. However, high-end six-axis force sensors still rely heavily on Swiss and Japanese suppliers.

2.5 Other Critical Components

- Robot Joint Modules: Localization rate 60%–70%, Chinese products cost roughly one-third of foreign alternatives.

- Mechanical Structures and Ball Screws: Localization rate above 85%, Chinese companies hold more than 60% global market share.

- AI Computing Chips: Localization rate around 30%–40%. High-end AI training chips still depend heavily on imported technology.

3. China’s Position in the Global Robotics Market

Industrial Robotics

China’s domestic robot makers now control nearly 60% of the home market and continue expanding internationally. Foreign manufacturers maintain a lead in high-precision industrial robotics, premium automotive automation, and advanced semiconductor manufacturing systems.

Humanoid Robotics

China has emerged as the dominant supplier in the global humanoid robotics market. Advantages include lower manufacturing costs, faster supply-chain coordination, strong domestic deployment demand, and aggressive scaling capacity. Chinese humanoid robot pricing is significantly below most Western competitors, creating pressure on global pricing across the sector.

Service and Logistics Robotics

China’s logistics and cleaning robot sectors are already globally competitive. Large domestic e-commerce and warehouse networks have provided ideal environments for deployment and product refinement.

4. Weaknesses and Industry Risks

Despite rapid progress, several structural weaknesses remain.

Dependence on High-End Imports

China still relies on overseas suppliers for several critical technologies, including high-end RV reducers, premium encoders, advanced six-axis force sensors, and high-performance AI chips.

Technology Gaps at the High End

Chinese reducers and motion systems have improved rapidly, but lifespan and precision still trail top Japanese products by an estimated 30%–50% in some categories. This gap becomes more important in demanding industrial environments requiring long-term reliability.

Trade and Intellectual Property Risks

As Chinese robotics exports expand globally, companies may face trade restrictions, tariff barriers, patent disputes, and supply-chain limitations. These risks could affect international growth strategies.

Margin Pressure From Intense Competition

Domestic competition has become increasingly aggressive, particularly in humanoid robotics and industrial automation. Price wars are already reducing gross margins for many manufacturers. The next phase of competition will likely focus more on reliability, software capability, AI integration, service ecosystems, and global support networks.

Industry Outlook

China’s robotics supply chain has moved from follower to major global competitor in less than two decades. Its advantages now include a complete manufacturing ecosystem, large-scale production capacity, fast product iteration, lower component costs, and massive domestic deployment opportunities.

For investors, several segments stand out as particularly important:

Defensive, Higher-Margin Segments

- Harmonic reducers

- Servo systems

- Vision sensors

- Cleaning robots

High-Growth Areas

- Humanoid robots

- Joint modules

- Roller screws

- Embodied AI systems

Higher-Risk Segments

- High-end RV reducers

- Advanced encoders

- AI computing chips

China’s robotics industry is still facing technical and geopolitical challenges, but its role in the global automation market is continuing to expand rapidly. Over the next several years, the country is expected to remain one of the most important drivers of growth, pricing and manufacturing scale in the global robotics sector.